Rates move. Goals change. And a home loan that fit last year may feel heavy today. If you are thinking about replacing your current mortgage with a new one, this guide will help you map the path with calm, clear steps. I will keep it simple, but not too simple. Numbers matter, and so does timing.

Recent months brought a bit of relief. According to reporting on average mortgage pricing, the average 30-year rate in the U.S. fell to 6.63% in early August, the lowest since April, with the 15-year at 5.75% after softer jobs data and a steady Fed stance. Many analysts still expect rates to hover above 6% for most of the year, with gradual easing possible by year end. You can see those figures in the coverage of the recent rate slide.

Homeowners noticed. In fact, as borrowing costs eased from near 8% last November to the mid-6% range, applications to replace loans jumped. Coverage notes that refinancing usually carries costs equal to about 3 to 6% of the loan amount, so it often makes sense when your new rate is at least 1 to 2% lower, or when you shorten the term to cut total interest. That guidance is discussed in recent reporting on whether to refinance as rates drop.

Another sign of momentum showed up when the 30-year rate touched about 6.13%, the lowest in roughly two years, and refinancing activity picked up. That shift is covered in reports on the jump in refinance applications. And a drop in bond yields suggests there could be more mild easing ahead, though a return to the very low rates during the early pandemic seems unlikely, as discussed in analysis tied to lower Treasury yields.

Small rate cuts save big.

So, should you act now? It depends on your goals, your equity, your credit, and your time horizon. Teams like Heart Mortgage help clients weigh these factors every day. Their approach is built around clarity and tailored options for first-time buyers, investors, and even clients who had trouble with approval in the past.

What mortgage refinancing is

Refinancing replaces your current home loan with a new one. The new loan pays off the old balance. You then make payments on the new terms. The main reasons people do it are simple:

- Lower the rate to reduce interest and sometimes the monthly payment.

- Change the term, such as 30 years to 15 years, to pay off faster.

- Switch the type, for example an adjustable rate to a fixed rate.

- Tap home equity in a cash-out refinance for repairs, debt payoff, or an investment.

- Remove a co-borrower after a life change or remove mortgage insurance when equity allows.

A quick story. A family in Orlando bought at a 7.8% rate last year. They kept the budget tight, but it pinched. With rates around the mid-6s, a new loan cut their payment by a few hundred dollars. That freed cash for their kids’ activities. It felt lighter. Not perfect, but better.

Key terms in plain language

- Interest rate: The cost to borrow, shown as a percentage. It drives your monthly payment and total interest paid.

- Loan term: How long you have to repay. Common terms are 30 or 15 years. Shorter terms raise payments but reduce total interest.

- Home equity: The part of the property you own. It is the home’s value minus what you owe. If your home is worth 400,000 and your loan is 300,000, you have 100,000 in equity.

Two other pieces help frame decisions:

- Loan-to-value (LTV): Your loan amount divided by your home value. A lower LTV can mean better pricing.

- Points: Optional upfront fees to lower your rate. One point is 1% of the loan amount.

Common types of refi and how they work

Rate-and-term refinance

This is the classic version. You swap your current loan for a new one with a different rate, a different term, or both. If the rate drops enough, your monthly cost and total interest can fall. If you shorten the term, you can wipe out years of payments, though your monthly bill can rise. There is no cash back at closing with this type.

Upside: Lower monthly payment, less interest over time, more predictable budgeting when moving to a fixed rate.

Risks: Closing costs add to the balance if you roll them in. Extending your term can increase total interest even if the monthly payment drops. Watch that.

Cash-out refinance

With enough equity, you can replace your loan with a larger one and take the difference in cash. People use the funds to renovate, pay off higher rate debts, or buy another property.

Upside: One loan, potentially lower rate than some other credit, and liquidity for goals.

Risks: Your balance increases. If you stretch the term, you could pay more interest over the life of the loan. Be careful not to drain too much equity, especially if you plan to sell within a few years.

Other paths

- Cash-in refinance: Bring extra cash to lower the balance and reach a better LTV or remove mortgage insurance.

- ARM to fixed: Trade an adjustable rate for the stability of a fixed payment.

- Term change: Go 30 to 20 or 15 years to slash total interest. Payments rise, but the finish line moves closer.

Heart Mortgage often helps clients compare fixed and variable options in plain terms. If you want a deeper read on that choice, the guide on fixed vs variable mortgage rates is helpful for framing risks and comfort level.

What it costs and how to test if it is worth it

Most homeowners pay closing costs between 3 and 6% of the loan amount when they switch loans, as noted in recent reporting on refinance decisions. Your list may include:

- Origination and processing fees.

- Appraisal and credit report fees.

- Title search and lender’s title insurance.

- Recording fees, taxes, and prepaid interest.

- Escrow setup for taxes and insurance.

- Points if you choose to buy down the rate.

Two quick ways to judge the math:

- Break-even time. Divide your total closing costs by the monthly savings. If costs are 6,000 and your payment drops by 250, your break-even is about 24 months. If you plan to keep the loan longer than that, it starts to make sense.

- Total interest check. Compare total interest left on your current loan to the total interest on the new loan. If you reset to 30 years after paying down for several years, your monthly payment might fall, but your total interest could rise. The total interest view keeps you honest.

If you like running your own numbers, try the Heart Mortgage refinance calculator. It puts the payment and break-even picture in one place.

When replacing your loan can be wise

- You can lower your rate by 1 to 2% or more. Even a single percentage point shift can cut thousands over time.

- You want to shorten the term. A 30-year to a 15-year swap can shrink total interest sharply.

- You need cash for a high return project. Renovations that raise value or a rental purchase can make a cash-out refi reasonable.

- Your ARM is about to adjust higher. A fixed rate can bring peace of mind.

- You can remove mortgage insurance. If equity is high enough, a new loan might remove PMI, trimming the monthly bill.

- Debt consolidation, done carefully. A lower rate is good, but do not turn short-term debt into decades of interest unless you plan to pay extra and finish early.

For borrowers who fit standard guidelines, conventional options are often a strong match. If you want to see how those work, check the overview of conventional loan programs that Heart Mortgage arranges.

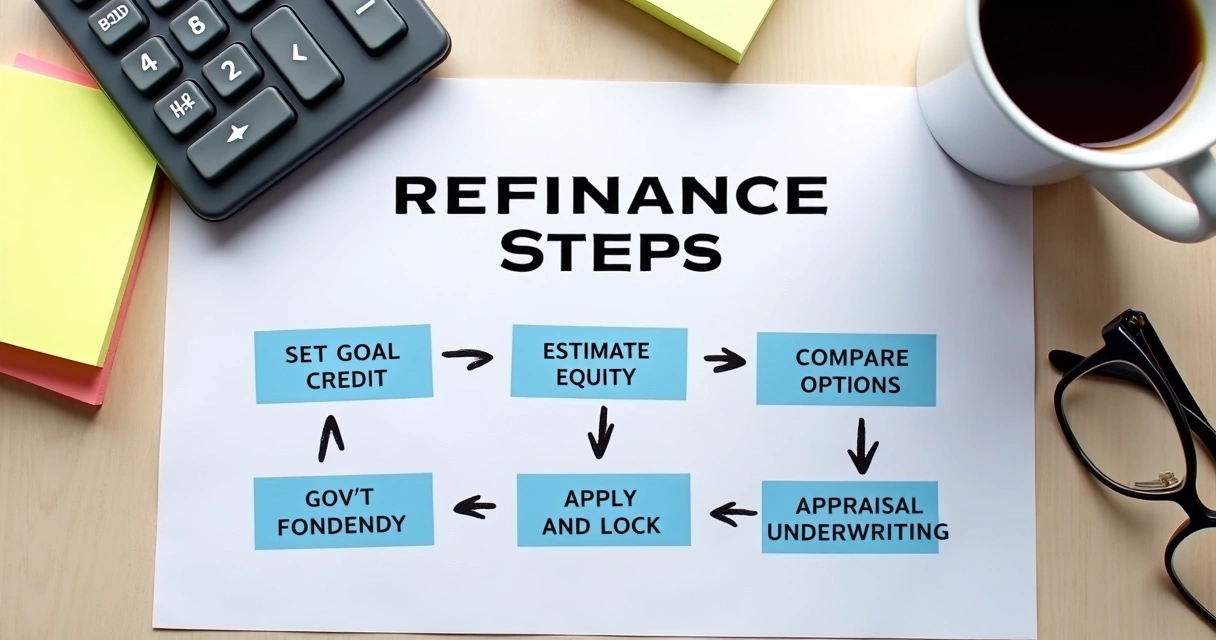

The refinance process step by step

- Set your goal. Payment relief, total interest savings, equity cash, or a faster payoff. Write it down. It guides every choice.

- Check your credit. Pull your reports. Fix errors. Pay down cards. A higher score can unlock a better rate.

- Estimate equity. Look at nearby sales and your current balance. If your LTV is under 80%, pricing usually improves.

- Gather documents. Pay stubs, W-2s or tax returns, bank statements, mortgage statement, insurance, and ID. If self-employed, be ready with business returns or other accepted income proof.

- Compare options and pricing. Review fixed and adjustable choices, costs, points, and terms. The Heart Mortgage mortgage rates blog can help you follow trends and context.

- Apply and lock. Submit your application. Once you like the terms, consider a rate lock to protect you while the loan is processed.

- Appraisal and underwriting. An appraiser estimates value. Underwriting confirms income, assets, and credit. You may need to explain a bank deposit or update a document. It is normal.

- Clear to close. Review your Closing Disclosure. Sign at closing. For many owner-occupied refis, you have a three day right to cancel after signing before funds disburse.

If you like a guided checklist, the Heart Mortgage article on 7 steps to refinance home safely lays out a simple path from goals to closing.

How to improve your approval odds and your rate

- Boost your score. Pay down credit cards to under 30% of limits. Make on-time payments for at least three months. Remove old disputes if asked.

- Stabilize your finances. Avoid new loans or credit cards right before you apply. Keep cash reserves steady.

- Lower your debt-to-income ratio. Pay off a small auto loan or a credit card if it helps. Even a small shift can move pricing.

- Document cleanly. Gather full statements, not partial screenshots. If you have large deposits, add a simple letter of explanation.

- Pick the right term. Shorter terms can come with lower rates. But only choose one you can live with during slow months.

- Consider timing. News moves markets. Rate locks protect you. If you are rate sensitive, follow updates like the recent report on lower averages and signals from bond yields.

Real-world scenarios

The payment cutter

Marcus bought a condo at a 7.7% rate. He now qualifies for 6.4%. He plans to keep the home at least four years. Closing costs are 5,500. His monthly payment falls by 260. Break-even sits at about 21 months. He crosses that line with time to spare. He goes ahead.

The equity builder

Sofia has a steady job and wants to be debt-free faster. She moves from a 30-year to a 15-year term. Her monthly payment is higher, but the total interest drops by six figures over the life of the loan. She sleeps better, even if the budget is snug. It is a values choice as much as a math choice.

The investor

A couple owns a rental with strong equity. A cash-out refi frees funds for a duplex down the street. Rents cover the higher payment. They accept a slightly higher rate to gain another door. It is not perfect, but the long-term plan matters more. For structure, they review conventional options that fit investment properties through Heart Mortgage and its conventional loan programs.

The home improver

A homeowner pulls cash to update a kitchen and repair a roof. The new payment is higher, but the upgrades raise the home’s value and comfort. He budgets carefully and adds extra principal to finish early. Not fancy, just steady.

How rates today shape decisions

Rates change daily. In late summer, the average 30-year slipped to near 6.6% on some reports, while other weeks saw moves closer to 6.1% with a clear jump in refi activity. Those shifts track with coverage of the dip to around 6.13% and the update on the 30-year at 6.63%. Bond markets hint that gradual declines could continue, though a return to the ultra-low rates from years past seems unlikely, as analysis tied to yields points out.

If you like tracking the broader picture, the Heart Mortgage mortgage rates blog covers moves and practical context. It is updated often and uses plain words where it can.

Small warnings and smart habits

- Do not restart the clock without a reason. A fresh 30-year can raise total interest unless your rate drop is significant or you plan to pay extra.

- Be wary of no-cost offers. Costs may be baked into a higher rate. Ask for a side-by-side quote with points, without points, and with lender credits.

- Mind the prepaids. Setting up a new escrow account is not really a fee, but it adds to your cash to close. You get credit back from the old escrow after funding.

- Keep an eye on term fit. If you are five years into a 30-year, ask for a 25-year option to avoid backsliding. Many lenders can match a custom term.

If you want a human guide who keeps the jargon to a minimum, that is the style at Heart Mortgage. The team, led by CEO Lee Dama, focuses on straight answers and timelines that feel realistic, not rushed for the sake of it.

Conclusion

Replacing your current mortgage can open room in your budget, cut long-run interest, or fund plans that move life forward. The idea is not to chase a headline rate. It is to match a loan to your goals and your time frame. Run the numbers. Check the break-even. Weigh the total interest. Then choose with calm.

If you are ready to see your options in writing, reach out to Heart Mortgage for a clear side-by-side. Use the refinance calculator, skim the 7 steps to refinance home safely, and ask for a quote matched to your profile. Simple, honest, and built around you.

Frequently asked questions

What is mortgage refinancing?

It is the process of replacing your current home loan with a new one. The new loan pays off the old balance, and you start making payments on the new rate and term. People do it to lower the rate, change the term, switch from adjustable to fixed, or take cash from equity for projects or investments.

How does refinancing a mortgage work?

You set a goal, compare options, apply, and lock a rate. An appraisal checks value, and underwriting reviews income, assets, and credit. At closing, you sign new documents, your old loan is paid off, and a new payment schedule begins. Many owner-occupied loans include a three day right to cancel after signing before funds are disbursed.

Is it worth it to refinance now?

It depends on your rate gap, costs, and how long you will keep the loan. As news reports show, average rates moved from about 8% last year to the mid-6% range, even touching near 6.13% for a time. Many advisors suggest a 1 to 2% reduction to offset costs that are often 3 to 6% of the loan. Use a break-even test and compare total interest before deciding.

What are the benefits of refinancing?

Common benefits include a lower monthly payment, less total interest, a faster payoff with a shorter term, fixed-rate stability if you currently have an adjustable rate, and access to equity for repairs, education, or another property. Risks include closing costs, a larger balance if you take cash, and the chance of increasing your total interest if you reset the clock to a longer term.

Where can I find the best refinance rates?

Rates change daily and vary by credit score, equity, loan size, and program. It helps to compare written quotes and ask for side-by-side options with and without points. To see trends and get a tailored quote, you can review the Heart Mortgage mortgage rates blog and request a scenario that fits your goals. When you are ready, connect with Heart Mortgage for a clear plan and a calm walk to closing.